sur Sektkellerei Schloss Wachenheim AG (isin : DE0007229007)

Schloss Wachenheim AG Sees Strong EBIT Growth Amid Lower Energy Costs

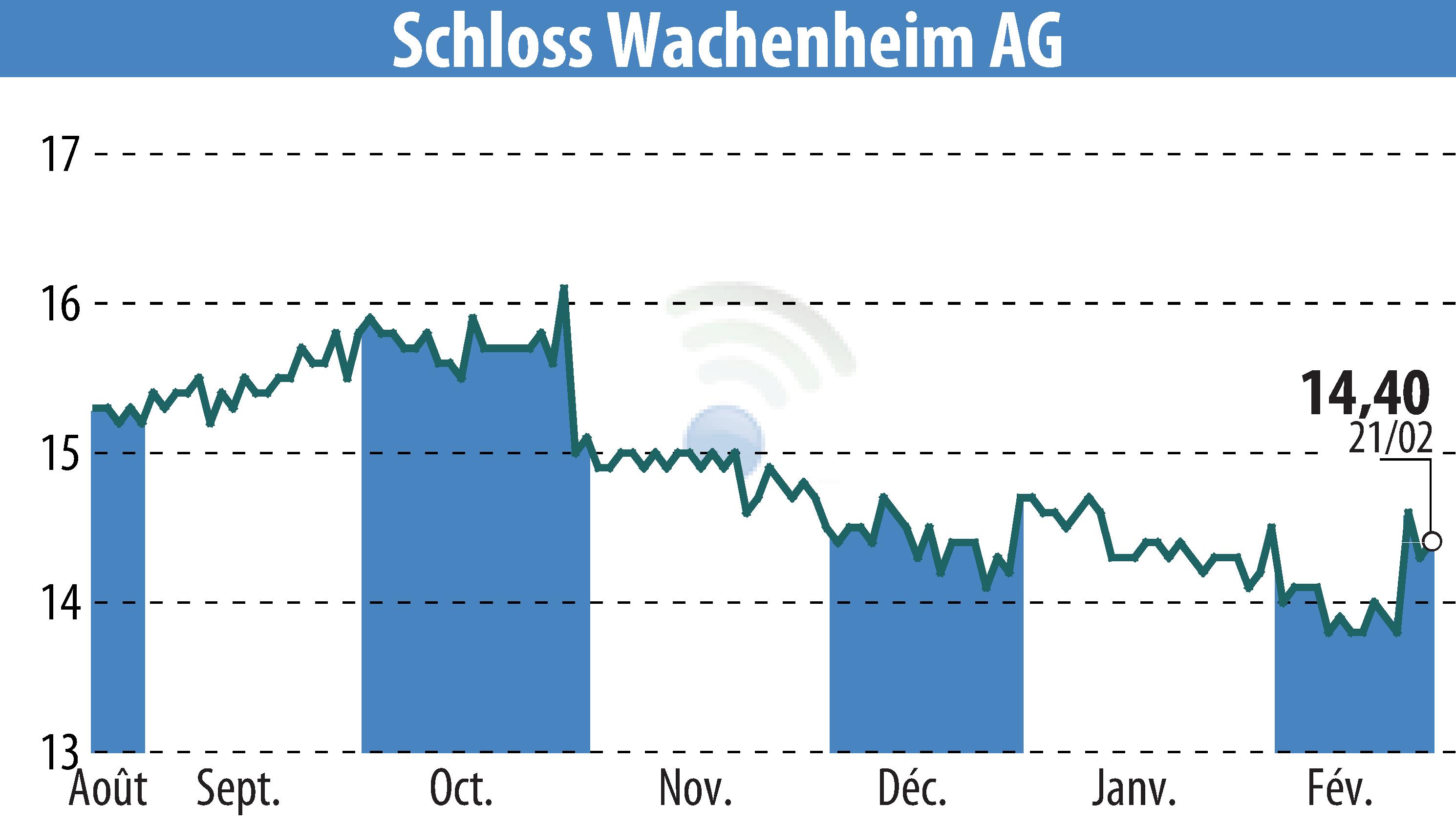

First Berlin Equity Research has reaffirmed its "Buy" recommendation for Schloss Wachenheim AG with a target price of €22. The research follows the Q2 2024/25 results, where the company saw a 3.8% increase in bottle sales in the crucial Christmas quarter. Group sales rose by 4.0% to €154.0 million, though this was slightly below forecasts.

EBIT experienced a significant increase of 31.5%, reaching €21.6 million, which exceeded expectations by 18.5%. Lower energy costs and changes in procurement costs played a role, particularly due to the favorable impact of the Polish currency appreciation.

Management expects sales growth to be at the lower end of the 5-7% guidance range from the previous annual report. EBIT and net profit forecasts remain steady at €31-€33 million and €20-€22 million, respectively.

R. E.

Copyright © 2025 FinanzWire, tous droits de reproduction et de représentation réservés.

Clause de non responsabilité : bien que puisées aux meilleures sources, les informations et analyses diffusées par FinanzWire sont fournies à titre indicatif et ne constituent en aucune manière une incitation à prendre position sur les marchés financiers.

Cliquez ici pour consulter le communiqué de presse ayant servi de base à la rédaction de cette brève

Voir toutes les actualités de Sektkellerei Schloss Wachenheim AG